As the world’s postpandemic economic order takes shape, the U.S. has emerged as an unexpected winner. Asian economies that fared relatively well during the pandemic—especially China, but also advanced economies such as Japan and Taiwan—have struggled to maintain steam.

The end of the pandemic-era export boom and Washington’s aggressive stimulus are two reasons. But the U.S. has another ace up its sleeve: big postpandemic immigration inflows .

Immigrants have helped cap inflationary pressures by expanding the workforce, despite falling birthrates, and will boost growth and public finances for years. Goldman Sachs estimated recently that above-trend immigration this year and last will boost potential growth by around 0.3 percentage point to 2.1% in 2024. Japan, meanwhile, struggled to expand at all in late 2023. Taiwan grew just 1.3% last year.

The migrant population has always been a touchy political issue in the U.S., but Northeast Asia’s rich nations have much bigger problems with it. As their populations age more rapidly, the consequences of that attitude are becoming more obvious. Pension systems, which depend on young workers to fund benefits, will become difficult to maintain. Falling populations will make exporters such as Taiwan and South Korea even more dependent on the vagaries of the chip price cycle. Higher government debt issuance could crowd out private investment or impinge on other urgent priorities such as national defense.

Taipei, Tokyo and Seoul recognize the problem and have begun to take steps to address it . But with populations already beginning to decline outright—and powerful political factions opposed to change—Asia could struggle to maintain much of its economic dynamism.

A growing body of research is highlighting the link not just between demography and economic growth but also between migration and growth specifically. A 2020 International Monetary Fund study found that, for advanced economies, a 1 percentage point rise in immigration relative to total employment tends to boost total output by almost 1% five years later. Strikingly, the model also found that productivity boosts delivered by higher immigration tended to raise the average income of native workers as well. One likely reason: Immigrants tend to bring different skill sets to the labor force , helping the overall economy grow more efficiently, and faster.

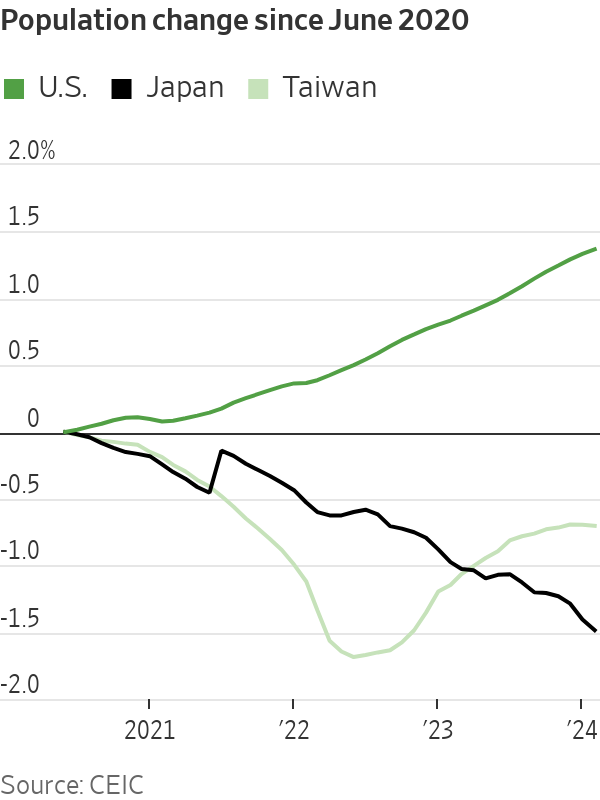

Japan’s population has already fallen by nearly 2% since 2019, while Taiwan’s is down nearly 1%. The U.S. population, on the other hand, is about 1.4% higher, according to U.S. Bureau of Economic Analysis data. More than half of that represents new foreign-born residents.

The long-term impact is likely to be substantial. In February, the nonpartisan Congressional Budget Office estimated that the U.S. economy will be about 2% larger in 2034 than it would have been without the current immigration surge. The federal budget deficit, according to the CBO’s reckoning, will also be nearly 1 percentage point lower as a share of the economy.

There have been more immediate effects, too. The U.S. probably owes its soft landing—declining inflation without a big rise in unemployment—in part to the influx of foreign workers who have, according to Federal Reserve officials, helped alleviate labor market pressure . For better or worse, America’s semiporous southern border can act as a safety valve when the economy overheats, drawing in low-skilled workers and making the emergence of a wage-price spiral and persistent inflation less likely.

The situation in Asia is very different. Japan, with its tightly controlled borders and shrinking labor force, has less policy flexibility. Even though the nation narrowly avoided recession last quarter and private consumption actually fell outright by 0.3%, the Bank of Japan elected to raise rates for the first time in 17 years this month. The main reason: a surprisingly muscular wage increase negotiated by unions this spring, totaling about 5%. Companies cited labor shortages as a major factor.

Aging Japan welcomes inflation, but not too much, because it would further cut into real consumption. Without more workers, it might continue to struggle to get that balance right. A 2019 International Money Fund working paper found that Japan’s “natural” rate of interest, i.e. the rate needed to maintain full employment and stable inflation, was probably already negative, in large part because of demographic headwinds.

If that is correct, Japan could find it difficult to avoid a recession in the coming quarters. It will also struggle to do anything about its mountain of public debt at about 260% of gross domestic product, already among the highest in the world.

Places such as Japan, South Korea and Taiwan especially need immigrant labor because birthrates are falling even faster than in the U.S. Japan’s total fertility rate—live births per woman—had already fallen to 1.3 by 2021, according to United Nations data. Taiwan’s was 1.1 while South Korea’s was a dismal 0.9. The U.S. is also well below the replacement rate of around two at 1.7 in 2021, but sustained immigration inflows have kept the U.S. labor force growing.

Japan and other aging Asian societies aren’t standing still. Last year, South Korea announced that it would issue a record number of visas——a 15-fold increase to 30,000—for foreign skilled workers. Japan in 2019 significantly expanded opportunities for low- or semiskilled workers in industries such as agriculture and nursing. It also unveiled a new fast-track long-term residence program for skilled professionals last year. And Taiwan in February signed a memorandum of understanding with New Delhi, paving the way for the recruitment of migrant labor from India.

But such incremental steps might not be nearly enough, especially if governments want to deliver on other priorities such as raising military spending or boosting domestic demand and diversifying the economy away from chips in Taiwan.

Time stands still for no one, but people are constantly moving. If Northeast Asia wants to stay competitive—and fast-growing—it needs to embrace that reality rather than ignore it.

Write to Nathaniel Taplin at nathaniel.taplin@wsj.com and Megha Mandavia at megha.mandavia@wsj.com