Private debt in the country remains a slow-burning bomb at the foundations of the Greek economy, according to an inaugural report entitled “Private Debt in the Greek Economy”, published by the Foundation for Economic & Industrial Research (IOBE) in collaboration with CEPAL.

“The total private debt continued to increase, driven by credit expansion and the accumulation of obligations to the public sector, while non-performing loans across the economy remained at high levels,” the report states in the introduction.

According to the report, 63.7% of total social security debt (around €32.3 billion) refers obligations created before, and as far back as 2010.

Private debt greater than GDP

Specifically, according to data for the third quarter of 2025, the total debt burden carried by households and businesses in the country broke every barrier, reaching the whopping figure of €407.6 billion (an amount corresponding to 164% of GDP), up from €392.8 billion in 2024.

This increase was fueled by credit expansion in loans (+€6.8 billion), loans held by servicers (+€4.5 billion), as well as the continued accumulation of new obligations to the tax authorities and social security funds (+€3.6 billion).

State remains the largest creditor

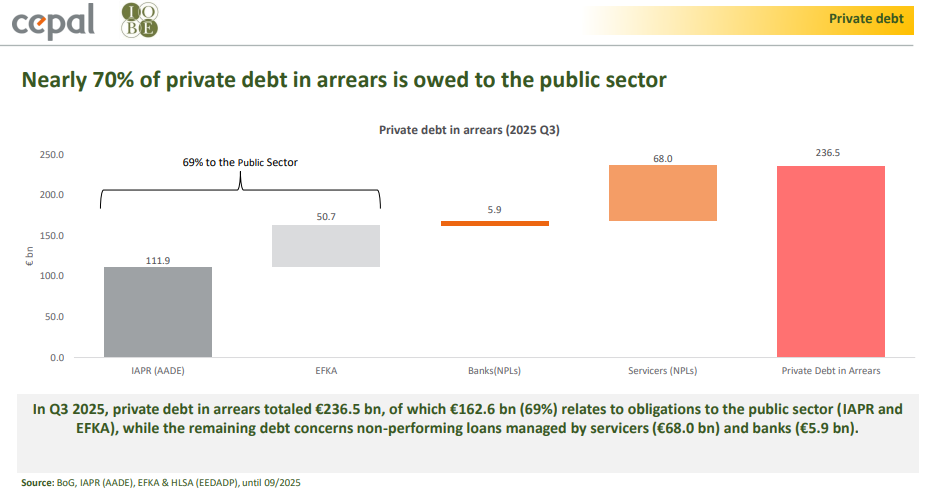

The most worrying element of this debt “snapshot” is that, out of the total €407.6 billion, €236.5 billion (that is, 58%) is deeply overdue debt. The state remains the main burden, with nearly 70% of overdue debts concern liabilities to the tax authority (AADE) and the main social security fund (EFKA). Tax debts remain at high levels at €111.9 billion, with legal entities holding the lion’s share (62%).