Carolina Lopez searched for therapy services for her autistic son, Ezekiel, who was then 3 years old. But every provider she called had a wait list. “There seemed to not be much I could do,” said Lopez, 33, a bank employee in Roselle Park, N.J.

A provider called the Perfect Child promised immediate treatment—and no out-of-pocket costs.

Beginning last July, workers came to her home several days a week to provide three to four hours of therapy for Ezekiel.

In April, she got the bill: $911,400.

The autism-therapy industry, once a tiny corner of pediatric care, has exploded into a multibillion-dollar business, fueled by rising diagnoses , new providers entering the market and laws requiring insurers to cover more services. It has also attracted predatory providers who bill for phantom services, pad hours and charge steep fees for care delivered by low-wage workers with minimal training.

The billing abuses run wide. Aetna said the number of investigations that found likely fraud or abusive billing by autism-therapy providers in its private-plan business shot up by 300% between 2024 and 2025—and is on track to rise by another 50% this year.

The issues detected by the insurer’s probes include poor documentation, billing for multiple services for the same hour and claiming to provide care at home addresses that don’t really exist, said Katerina Guerraz, Aetna’s chief operating officer.

“We’re seeing just a massive inflation,” especially when providers are not in-network, Guerraz said.

In bills reviewed by The Wall Street Journal, a daily charge for one child reached more than $30,000.

When insurers refuse to pay what they consider outlandish or unjustified claims, some providers pursue people directly, dragging families into financial and legal turmoil and disrupting care for disabled children. In Lopez’s case, her insurer had rejected claims, and the therapy provider billed her instead.

Simcha Bendet, the founder of Brooklyn, N.Y.-based the Perfect Child, which says it provides home-based autism therapy in 30 states, didn’t respond to phone calls and email inquiries. The company’s website provides little information about the structure or leadership of the business. A person answering the phone last month at the company’s main number instructed the Journal to email written questions, but the company still provided no response.

On Monday, a man answering the door at the residential Brooklyn address listed on the company’s corporate filings who appeared to be Bendet denied he was him, said he couldn’t help and closed the door. Phone numbers associated with the Perfect Child were disconnected or answered with an automated recording saying no one was available, including some used to conduct business as recently as Friday.

Former employees of the Perfect Child said the company’s high prices gave it leverage in negotiations with insurers, and while it didn’t join health-plan networks it often contracted to take single cases. A video on the company website says its approach allowed it to provide services fast and early, when they are most effective.

Autism-therapy spending has become one of the fastest-growing healthcare expenses for many private insurance plans, insurers, employers and auditors say. The boom has also made the therapy one of Medicaid’s fastest growing segments , according to a Journal investigation published in March. Medicaid claims data showed providers billed as much as $340,000 per patient a year, the Journal reported.

In the private insurance sector, annual spending on hands-on autism therapy for about 40 large employers covering 3.5 million people doubled to $108 million from 2021 to 2025, according to claims data analyzed by the Health Transformation Alliance. The coalition, which helps companies including Walgreens and American Express track and manage medical spending, said that reflects more patients, more hours of service and higher prices.

Anthony Margello looked at a bill for autism therapy for his daughter Cecilia, center, as she and his other daughter, Olivia, ate dinner at home in Columbus, Ohio. Brian Kaiser for WSJ

Cecilia used an iPad in her bedroom. Brian Kaiser for WSJ

Those rising costs help drive higher premiums for all workers and employers. Employer-backed insurance coverage for a family cost a total of nearly $27,000 on average in 2025, up 26% compared with five years earlier, according to KFF, a health research nonprofit.

For some employers, autism therapy has become an even bigger expense than routine doctor visits and chemotherapy, according to SmartLight Analytics, a data firm that monitors medical costs for employers. “It’s shocking,” said Asha George, the firm’s chief executive. “It’s all recent.”

Blue Cross Blue Shield of Arizona said spending per autism patient has risen by about 30% over the past two years, and much of the increase is due to a few dozen providers billing large numbers of hours for each child—what amounts to full-time workweeks of therapy.

“When you look at the number of units that some of these providers are billing for, they’d have to be doing these services 24 hours a day, seven days a week,” said Pam Kehaly, chief executive of the nonprofit insurer, which is investigating a growing number of questionable billings.

Aetna said it plans to launch a program this year to steer patients to autism-therapy providers that get better results and bill in a manner it considers appropriate.

Investors have poured into the business, which has been growing quickly and has few regulations. In many states, anyone can open an autism therapy clinic with little more than hired staff—far less scrutiny than a daycare center faces. Indiana, a top state for autism therapy, requires licensing applications and fire and safety inspections for daycares, but not autism-therapy companies.

Indiana officials plan to announce this week the state is pausing new enrollments of autism-therapy providers with its Medicaid program, said Marcus Barlow, a senior official at the state agency overseeing Medicaid.

Autism therapy, or applied behavior analysis, is commonly given to young children. Sessions of ABA, as it is called, often involve practicing chores, communication and social interaction at clinics or in patients’ homes.

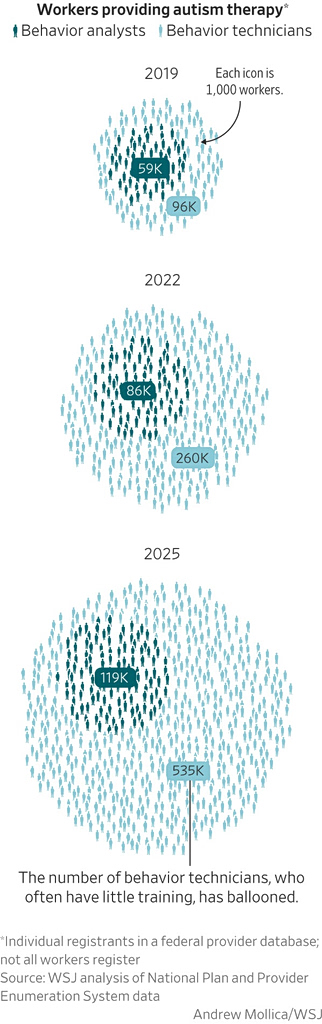

Most of the therapy is delivered by behavior technicians, who in many states need little more than a high-school degree and often earn as little as $20 an hour. By the end of 2025, about 535,000 people were registered as behavior technicians in a federal database of healthcare providers, an increase of 457% from 2019, an analysis by the Journal found.

The front-line workers are overseen by behavior analysts, more highly trained professionals who often have master’s degrees and licenses and can supervise multiple technicians.

One day’s bill: $30,500

Lopez’s son, Ezekiel, began receiving autism therapy from the Perfect Child last summer. Soon after, her insurer, Highmark, began receiving bills for $15,000 or more a day, insurance records show.

The bills came mostly from Kiedga LLC, one of more than 100 limited-liability companies linked through medical-provider registration records to the Perfect Child, its founder or the Brooklyn address on its corporate filings.

On Aug. 18, for example, a behavior technician spent a total of 70 minutes with Ezekiel, working on a puzzle and playing with educational toys, according to a medical record reviewed by the Journal.

For the day, Kiedga submitted a claim to Highmark for $15,200 for the technician and another $15,300 for that person’s supervisor—a total of $30,500, or $436 a minute for Ezekiel’s care. The insurer paid about $15,000 to resolve it.

Other days, the Perfect Child billed for services, but no one showed up to provide them, according to insurance records and Lopez. She also said she didn’t take advantage of openings that became available with another autism-therapy provider, where Ezekiel had been waitlisted, because she thought she would be getting services from the Perfect Child.

In February, Lopez got a call from the Perfect Child saying Highmark had stopped paying the claims—six months earlier. Lopez said Highmark eventually told her the autism-therapy company hadn’t provided requested documentation.

Lopez said she was unexpectedly billed over $900,000 for Ezekiel’s autism therapy. Sasha Maslov for WSJ

In March, the Perfect Child asked Lopez to file an appeal with Highmark and mentioned it was an out-of-network provider, meaning it had no contract with the insurer that set prices, an email thread reviewed by the Journal shows. Lopez replied that New Jersey law requires providers to disclose out-of-network status upfront and questioned the high charges.

Two weeks later, in April, the company asked her to pay the $911,400 bill and then followed up with another bill shortly after indicating the amount due had grown to $916,000. Payment options included using the Zelle money app. A debt collector for the Perfect Child told Lopez her insurer was at fault in a call she recorded the next day.

“They know there are parents like me who need the help, and we’re so desperate for it,” said Lopez. “You’re trying to do what’s right for your kid, and there’s people who are taking advantage of this.”

The Perfect Child therapists stopped coming in March. Now, Lopez said, she and Ezekiel are taking a break from autism therapy altogether, citing the experience with the Perfect Child.

Kurt Spear, the head of financial investigations at Highmark, declined to comment on the Perfect Child, citing an active investigation of the company. Spear said suspicious billings to Highmark from out-of-network autism therapy providers “is in the multimillion dollars at this point,” and that Highmark clients receiving questionable bills should contact the insurer.

The Journal spoke to 10 other parents who received five-figure-plus surprise bills from the Perfect Child, including some who have been sued in an effort to collect payments.

Legal challenges

Out-of-network medical bills have long created headaches for consumers. With no insurer contract to constrain them, providers can set rates as high as they want. Patients can wind up on the hook for big charges if insurers deny the claims or pay out less than what’s billed.

For years, consumers faced unexpected bills from out-of-network doctors staffing in-network hospitals. A 2020 law called the No Surprises Act now protects consumers in that situation—but does little to guard against other types of medical bills.

“There’s nothing that sets what a provider can bill,” said Barry Alexander, a shareholder at the Polsinelli law firm, adding that those prices are often a starting point for negotiations with insurers.

Health insurers and the employers that fund employees’ coverage are required to cover autism care by state and federal laws meant to ensure access to mental-health services.

When providers submit high bills, insurers often attempt to negotiate lower prices and can investigate and sanction providers suspected of fraud. Such disputes can end up in litigation when settlements aren’t reached.

Publix Super Markets, a major grocer in the southern U.S., sued ABA Centers, a large provider operating about 50 centers in 15 states, last year in federal court. Publix alleged ABA Centers fraudulently billed its health plan nearly $32 million over several years by unjustly inflating charges and double-billing for some services, among other things, in the ongoing case.

According to court records, ABA Centers billed Publix’s health plan up to $1,320 an hour for routine autism-therapy services. Publix typically paid 60% of the charges, or $792 an hour, for claims it approved, court records say. For out-of-network services, health plans commonly don’t cover the entire bill, leaving the rest to the patient.

The national average major insurers pay an in-network provider for such services is $89 an hour, according to an analysis of insurers’ pricing data performed for the Journal by health-tech company Turquoise.

ABA Centers also sued Publix, accusing the grocer of failing to pay for care its health-plan administrators had authorized. In a press release last year, ABA Centers said Publix cut off its payments 10 months before the lawsuits, but that it continued to provide services to Publix-covered families that the health-plan approved. ABA Centers declined to comment, and Publix didn’t respond to a request for comment.

Web of companies

Bendet, the entrepreneur who founded the Perfect Child in 2018, said in a video posted on the company’s website that he became interested in autism after going on camp trips with a friend and the friend’s autistic brother as a 16-year-old.

The company used social media to recruit workers and target patients, with online advertisements on Facebook, parents and former employees said. It quickly grew to service several hundred children, said former employees who worked for the company until 2023. One of them said it generated millions of dollars in annual profit.

In May, Bendet closed on the $3.1 million purchase of a Brooklyn home, one of a number of real-estate purchases he has made as the Perfect Child grew, property records show.

Its workers said they were offered significantly higher wages than competitors paid and said some scheduling was done over WhatsApp. Parents were often told services would be provided at little or no out-of-pocket cost, and they could start immediately.

The Perfect Child then billed health plans rates far higher than is typical, up to about $13,000 an hour, according to insurance records viewed by the Journal. That’s roughly 150 times the average rate paid for in-network providers, according to the Turquoise data.

At times, insurers rejected claims submitted by the Perfect Child after questioning the bills.

Those bills came from companies with names such as Junior Boom ABA LLC and Cedar Eye Therapy LLC, among others the Journal linked to the Perfect Child. Provider registration records used by insurers and the government make clear the companies are part of the Perfect Child’s network.

Insurers say the variety of company names makes it harder to track questionable billers. UnitedHealth Group, which insured some Perfect Child patients, said “it is not at all uncommon to see ABA providers change names and” tax identifiers to avoid detection of potentially fraudulent billing.

When insurers rejected those prices, the company discharged patients and pressured parents to appeal the insurers’ decisions. It sent large bills to families that didn’t comply and aggressively pursued purported debts.

The company and its affiliates have sued at least 19 patient families and employers in an effort to extract payments since late 2024, according to court records. Bendet’s companies were often represented by his brother, attorney Binyomin Bendet, an unsuccessful 2021 candidate for New York City Council. Binyomin Bendet didn’t respond to requests for comment.

The suits alleged health-plan sponsors including Teva Pharmaceuticals, a construction workers union in Newburgh, N.Y., and the Mitchell Companies, a Meridien, Miss.-based distributor and manufacturer, failed to pay for services they had agreed to cover.

Affiliates of the Perfect Child billed the Mitchell Companies $11 million for autism therapy for just two patients over 13 months, according to court records. In a court filing, the Mitchell Companies accused the Perfect Child of fraudulent billing, including a series of claims that would amount to more than 11 hours of service every day in June 2025 for one child, whose parents said in reality got about four hours of treatment four days a week. Lawyers for the Mitchell Companies declined to comment.

$10,000 ‘babysitter’

Russell Michels, of Plant City, Fla., said his health plan, administered by a unit of Elevance Health, paid hundreds of thousands of dollars for about nine months of autism therapy by affiliates of the Perfect Child for his son, who is now 7, which he said included activities like pushing him on a swing in the backyard. He said the company scheduled three-hour therapy visits at his home three or four days a week.

Elevance sent Michels a series of explanation-of-benefit statements that listed bills from the Perfect Child totaling $510,000 for services performed in August and September of 2024. The records said the health plan paid amounts totaling $358,500 for those services, with payments of $10,000 for many single dates of service.

“If I wanted a babysitter for $10,000 a pop, I would have found me one,” Michels said.

Michels said his family quit the Perfect Child at the end of September 2024. The Perfect Child sued him in Florida court earlier this year, claiming he owed another $108,000. Michels disputed the allegations and said he is representing himself in the ongoing case because he can’t afford a lawyer.

In a statement, Elevance said it was taking action to combat fraud, waste and abuse in the autism therapy space and protect members of the health plans it oversees.

In 2023, the insurer unit of UnitedHealth Group began to question bills from an affiliate of the Perfect Child it received for a now 10-year-old Columbus, Ohio, patient named Cecilia Margello. The insurer asked for more details about the services. A Perfect Child representative told the patient’s mother, Ashley Margello, it had sent the records on time; UnitedHealth told her it never received them.

The dispute took a year. UnitedHealth eventually denied months of claims, and wrote in a letter that it had suspended any future payments to a behavior analyst working for the company “for misrepresentation of services.”

“We are unable to work with that insurance plan anymore,” a Perfect Child representative said in an April 2024 phone call, according to a recording reviewed by the Journal. The representative said on the recording there would be no charge and promised to have someone prepare a discharge plan.

Cecilia’s then-behavior technician said in an interview that the Perfect Child abruptly cut off all three children she treated around the same time over insurance problems. Margello said she never did receive the discharge plan—but did get a $35,000 bill two years later, this April.

The Perfect Child sometimes billed families for huge amounts even when it had agreed to cap charges. Annette Valle, a part-time hairdresser from Deltona, Fla., then earning about $300 a week, submitted a financial assistance form to the Perfect Child when she signed her daughter up in the summer of 2024.

A Perfect Child representative told her in an email reviewed by the Journal that she would owe just $146 a month, on top of what her insurer, Cigna, would pay the provider. But, when Cigna stopped paying last fall, the company abandoned that agreement, sending a series of four bills totaling over $160,000.

Valle said she hasn’t signed her daughter, who is now 16, up for any more autism-therapy services since.

“I was afraid to,” Valle said. “We’re already in this mess and the last thing you want to do is end up with outstanding bills again.”

Write to Christopher Weaver at Christopher.Weaver@wsj.com and Anna Wilde Mathews at Anna.Mathews@wsj.com